Global Price Escalation: Inflationary pressures

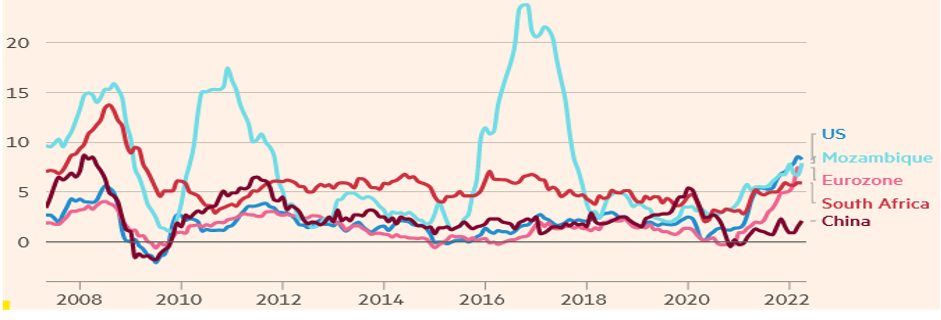

The high level of inflation becomes geographically broad, with inflation reaching its highest level in a decade in many countries. Consumer price growth has even begun to rise in Asia, a region that recently was an exception to the world standard.

Caption: The chart above shows the percentage change in the level of inflation (consumer price index) on an annual basis from 2008 to March 2022

Among the causes influencing the worsening of global prices are as follow: the excessive level of liquidity injected into developed countries during the pandemic to ensure that economies continued to flow in a period of relatively low production; subsequently, the reopening of economies after a long period of restrictive measures to contain COVID-19 amid a context that many industries such as oil industry found it difficult to meet the (expected) excessive demand. Oil industry saw a divestment in the highest period of the pandemic, due to weakened demand and incentives for new energy transition trends, from the use of fossil energy to renewable energy. This imbalance between demand (high) and supply (low), led oil prices and its products to be boosted.

The increase in fuel prices creates a rise in the prices of goods, food, and chain services, affecting the price of transport of passengers and goods, which consequently tends to increase the price of such goods. This raises concerns about an energy crisis and a global food crisis.

At the moment, the main discussion between policymakers and economists remains focused on how long inflation will last. A few months ago, many expected the increase to be short-lived for monetary policy to have a major impact, with higher rates taking time to infiltrate economies. However, the geopolitical conflict between Russia and Ukraine, along with signs that inflationary pressures have become broader, has exacerbated fears that inflation may be stricter than expected.

Energy crisis: Impact of Russia-Ukraine conflict on energy sector

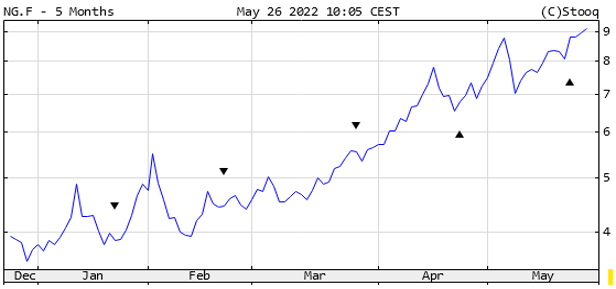

The Russia-Ukraine geopolitical conflict has exacerbated the appreciative trend of energy sector worldwide, but above all in Europe, due to Russia’s high dependence on Europe for the supply of natural gas. This burden on the EU became evident with the high level of devaluation of the euro after Russia’s invasion of Ukraine.

Caption: The chart above illustrates the trajectory of the EUR/USD exchange rate, from January to May 26, 2022. The main objective is to demonstrate the depreciative trend of the euro against the US dollar as a result of the geopolitical conflict between Russia and Ukraine.

Caption: The chart above illustrates the trajectory of natural gas, in USD/, from January to May 26, 2022. The main objective is to demonstrate the appreciative trend of natural gas, and the worsening of its appreciation after Russia’s invasion of Ukraine in the second half of February.

As Russia is among the five largest producers of oil and its products worldwide, the sanctions imposed on Russia, which limit its commercial activity, worsen the growing global inflationary trend.

However, after the Western powers imposed financial sanctions on Russia, President Putin announced that the “hostile” countries would have to pay for the gas in the Russian currency, Ruble.

The Russian state-owned energy company Gazprom imposed on Poland and Bulgaria that payments be made in rubles.

Many other EU countries suffered the same problem in mid-May, when payments were due.

Ruble payments instead of euros strengthened the Russian currency, and would benefit its economy in a way.

Caption: The chart above illustrates the trajectory of the USD/rub exchange rate in the period from June 2021 to May 20, 2022. Main objective, demonstrate the appreciative trend of the Russian Ruble after the beginning of the invasion in February to May.

Caption: The chart above illustrates the trajectory of the EUR/rub exchange rate in the period from June 2021 to May 20, 2022. Main objective, to demonstrate the appreciative trend of the Russian Ruble after the beginning of the invasion in February to May 2022.

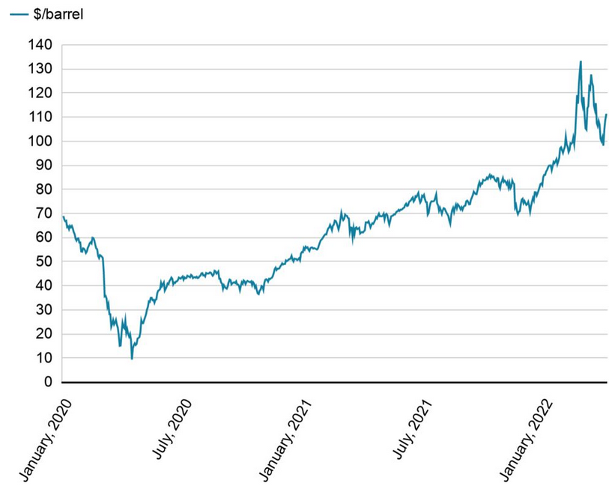

Crude oil prices (Brent) have been rising but steadily, i.e. without major fluctuations, between USD 100-115 a barrel from April to May, after reaching a 13-year high in early May, after the invasion, at the level of USD130 a barrel.

The chart above illustrates the change in the price of Oil (Brent), in dollars per barrel, since the beginning of 2022. The main objective is to illustrate the oil appreciation in the second half of the first quarter of 2022, its subsequent relative stability between USD100-115/barrel from April to May 2022.

The chart above illustrates the change in the price of Oil (Brent), in dollars per barrel, on an annual basis, from January 2020 to January 2022. Main objective, to illustrate the appreciative trend of oil, after the outbreak of the COVID-19 pandemic in 2020, the worsening of this appreciative trend with the geopolitical Russia-Ukraine conflict.

The relative stability of oil prices, between the levels of USD100-115/barrel, can be justified by the fact that the US announced that it would release about 1 million barrels/day of its reserves to supply excessive demand and reduce energy prices for a period of six months. Another factor that may be contributing to this relative stability is the fact that China, which is one of the largest energy importers/consumers, has recently gone into lockdown, which has caused a downward revision of energy demand and has consequently reduced fuel price volatility.

Commodity Market: Main developments, focus on wheat

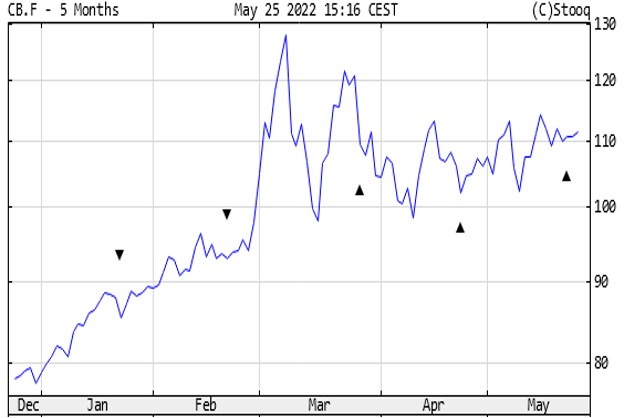

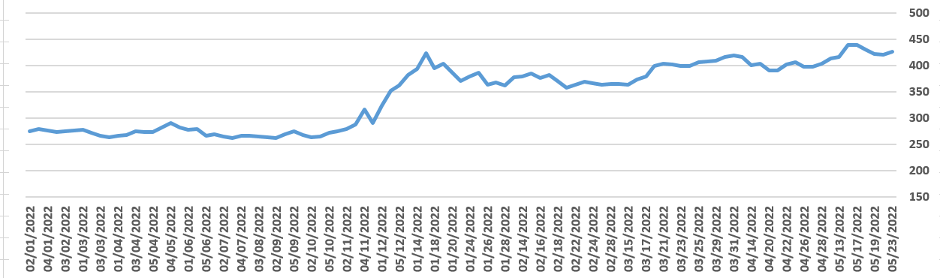

Russia and Ukraine are among the largest producers and exporters of wheat and fertilisers. However, the geopolitical conflict between these two countries, along with the sanctions imposed on Russia, has exacerbated the constraint on the food supply chain in international market, thus generating volatility in wheat prices and concerns about a global food crisis. As a result, the price of milling wheat has recently reached the level of EUR 438.25 per tonne, coming from a level below EUR 300 per tonne in January of this year.

Evolution of wheat price (in EUR/Ton)

The chart above illustrates the change in the price of Wheat, in euro/ tonne, on an annual basis, from January to May 2022. The main objective is to illustrate the appreciative trend of wheat, after the invasion of Russia in Ukraine.

This has a very negative impact on our country, due to our strong dependence on food imports.

If our country’s grain reserves are not robust, the price of bread and other food can be expected to rise, as the country will have to import more grains at current market prices.

Another factor that could also contribute to the worsening of wheat prices is the latest announcement by the Indian Government to partially ban exports of wheat to other Asian countries in order to ensure domestic consumption and generate greater grain reserves in India. Although the bulk of India’s exports are mainly to Asian countries, this measure by India has an effect on wheat prices in the international market.

Valuation of extractive products and possible benefits for African economies

With the European energy crisis and the European Union’s decision to classify gas as a green energy, an opportunity can be envisaged that will benefit African economies in the years to come. And Mozambique may become one of the countries that most benefits from the growing demand for this commodity, given the colossal size of gas reserves that our country has.

With the current geopolitical conflict between Russia and Ukraine, Europe feels a greater need to reduce its level of dependence on Russia’s gas. With this, investments in gas projects in Africa are expected to increase, to develop more resources to be consumed in Africa and to be exported to Europe.

However, this projection is not linear, for Mozambique and other African countries to attract a significant share of these investments, an enabling business and investment environment, including a transparent and clear legislative framework, should be developed.

Unfortunately, African countries are not currently prepared to meet Europe’s demand. Nigeria, for example, which is another country rich in extractive resources, continues to import oil because it holds the raw material, but lacks infrastructure to refine the oil so that it is ready for use.

Therefore, African notions will only be able to benefit from the continent’s growing gas demand in the coming years as more investments are made on the continent.

Interbank Money Market: Increased cost of credit

The Monetary Policy Committee (CPMO) of Bank of Mozambique decided to maintain the monetary policy interest rate, MIMO rate, at 15.25%. This decision is underpinned by the prospects of maintaining inflation at one digit in the medium term, despite the high risks and uncertainties associated with these projections, with emphasis on the effects of geopolitical tension in Europe. Meanwhile, in the short term, inflation will remain high, reflecting the impact of the adjustment in the prices of administered goods.

According to the private sector, the increase in the reference interest rate benefits gasoline companies and harms the productive sector, in a context in which the Bank of Mozambique reiterated that the measure taken aims to prevent the problems that the economy would face with the general price increase.

However, CTA states that it sees no relationship between interest rates and inflation. Business industry also foresees significant consequences for small and medium-sized enterprises with the implementation of the measure.

Economists and the business sector argue that the major problem in raising the reference interest rate is the formula for calculating the Prime Rate (which has already increased from 18.60% to 19.10% at the beginning of May), a measure that prevents the productive sector from being more competitive in relation to other markets.

It is also argued that there is little room for manoeuvre to reduce the current level of the reference interest rate in the interbank market, which is seen as high by several players, especially companies operating in the domestic market, despite the exogenous facts that are difficult to change.

It is added that Mozambique should have been more in expectation of what would happen over time, giving as an example the country’s participation in the fuel sector, in which large exporters proposed to restore fuel production worldwide, in addition to expectations regarding the Russian-Ukrainian tensions that may have a brief and positive outcome, emphasizing that there was a haste on the side of the Central Bank.

Resumption of foreign financial assistance: aid effectiveness, timeliness/timing, challenges, opportunities and perspectives direct/indirect impacts

One of the prominent issues for the national economy in the first half of the year is the resumption of IMF financial assistance to Mozambique, considered by many economists as the “Oxygen Balloon” for the country, since it will help to relieve the pressures on the budget, and above all on public spending, because it will help to increase financial margin of the State, conveying a message of confidence to investors and partner countries.

The agreement with IMF, according to economists, will make more accessible financial resources available to the country on favorable terms, since the financial envelope announced by this organization is interest-free and has a relatively long grace period and amortization period.

IMF leadership stated that the objective is to support a set of government reforms aimed at ensuring economic recovery, highlighting the importance of the public finance management sectors.

During the negotiations, IMF advocated a series of tax and VAT policy reforms, as well as the creation of a sovereign fund for mineral resource revenues.

With regard to VAT reform, the premise is based on the fact that the country’s tax burden is a blocking factor to the economy itself, coupled with the fact that Mozambique has one of the highest VAT rates in Southern Africa, with the private sector for some time now calling for a reduction in this tax.

In May, Mozambique then began a new phase with the resumption of foreign financing to support the State Budget by IMF, approving US $470 million, with a 10-year debt grace period and whose interest is basically zero.

The amount will be disbursed by IMF for the implementation of an Extended Financing Programme by 2025, with the ambition of supporting the country to ensure sustainability, inclusive growth and long-term macroeconomic stability.

At the end of the country financing programme, three years from now, IMF expects to see a country with stable national economic growth, balanced levels of cost of living, a safeguarded household income and good governance.

The program also provides for the creation of a budgetary space for the financing of social protection programs, covering more than 30,000 households (families) per year, an average of 150,000 people, Mozambican Government said.

Furthermore, to promote job creation, improve the business environment in the country, and increase the diversification of the economy, the IMF’s new financial program also provides financing to the private sector, also as a way to replace imports with domestically produced products.

On the other hand, Mozambique’s government also expects the World Bank to start financing the State Budget again this year, with an initial amount of about 300 million dollars, according to the Minister of Economy and Finance.

If the World Bank’s financing is implemented, Mozambican State will have a total of US $770 million for the year 2022.

However, economists also argue that the country must act with caution because, despite conveying a message of hope, for now, the 470 million dollars announced, to be disbursed for a period of three years, are scarce for the “deficits” that Mozambique faces.

Financial Inclusion Report of the Bank of Mozambique

- Key Findings/Conclusions

For 2021, with regard to banking, measured by the number of bank accounts per 1000 adults, there was an increase of 3.40% compared to 2020 (an increase of 176,501 accounts), which led to the expansion of electronic money accounts.

Rural financing has made significant progress. MITADER’s “One District One Bank” initiative provided, between 2016 and 2021, the opening of 45 bank branches in the districts. In turn, the Project SUSTENTA, in the agrarian campaign 2020/2021, benefited 103 districts in eight provinces of the country and covered, directly and indirectly, a total of 291,241 beneficiaries.

In the capital market, market capitalization showed a growth rate of 18.90% compared to 2020.

In the light of the digitization of state payments, it rose to just over 184,000 pensioners who received their pensions via bank transfers, at the level of the Single Centralized Pension Payment System Project, being implemented by the INPS, which raises to 95% of pensioners receiving their pensions via transfers. Similarly, about 17,000 beneficiaries of Digital Social Protection Payments received digital transfers from INAS.

- Prevailing Challenges

Despite the remarkable advances in the Financial Inclusion Index, some challenges persist, such as:

- Regulation of KYC (Know Your Client) by levels, whose approval is conditional on the completion of the review of Law No. 14/2013, of August 12, the Law of Prevention and Fight Against Money Laundering and Financing of Terrorism.

- Framework for licensing and supervision of fintechs, prepared the proposal for regulations aimed at creating and establishing the legal regime for technology-based financial service providers (fintech) – to be approved by BM.

- Bank Accounts General System, prepared the proposal for a Law that aims, among others: (i) reduce the minimum age for opening an account, from the current 21 to 18 years old and (ii) institutionalize the basic or simplified bank account, focusing on the most needy populations and rural areas – it needs approval.